The EP's Payment Adjustment will be negative (i.e. "penalty"), positive (i.e "bonus"), or neutral (i.e. "no adjustment"). This percent change will be recognized on Medicare claims filed by the NPI + TIN combination, two years after the reporting period.

Keep in mind, EPs are defined by their unique NPI + TIN combination, meaning any NPI may have several Payment Adjustments, depending on how many TINs they bill under. For example, if a given NPI files claims with CMS using 4 different TINs, they will receive 4 separate Payment Adjustments. This provides segregation between employers, such that the payment adjustment from one TIN will not affect another TIN's future claims.

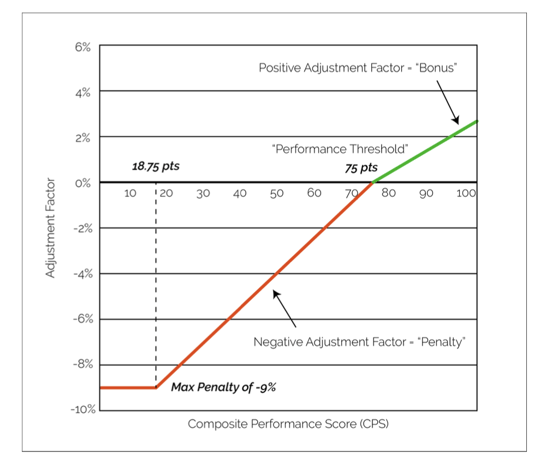

The Payment Adjustment is determined by the EP's Composite Performance Score. This is a nonlinear relationship across the entire CPS range (see chart below). While predicting any specific Payment Adjustment is difficult, the table below illustrates some helpful "mile markers", connecting specific payment adjustments to specific Composite Performance Scores.

|

Payment Adjustment |

Composite Performance Score |

Common Name |

|

-9% |

0 - 18.75 |

Max Penalty |

|

Linear sliding scale |

18.76 - 74.99 |

|

|

0% |

75 (same in 2022) |

Performance Threshold |

|

Linear sliding scale |

75.01 - 99.99 |

|

|

+9% (theoretical max)* |

100 |

Maximum Bonus |

*Theoretical max bonus is a function of the amount raised from the EPs paying a penalty via negative payment adjustments. Estimates for max bonus will likely be closer to +3%.